I wanted to take some time to talk about the action this week in Kraft Heinz (KHC). On Thursday, the company reported earnings. Despite significant progress on the cost-cutting front, the headlines were bad. Q4 net sales were down 3.7%. Susquehanna issued a downgrade due to “slower EBITDA growth and delayed deal-making,” as was reported in this Barron’s blog post. Analysts Pablo Zuanic and Aatish Shah even went so far as to predict “little upside in the year ahead.” As a result, the stock finished down $3.82 or 4.2% on Thursday, February 16.

What a difference a day makes.

Turns out that not only is “deal-making” in the air, but the ever-acquisitive Kraft Heinz management had already approached Unilever (a list of their brands that claims 2.5 billion daily customers can be found here) about one of the biggest deals in the history of the consumer food and beverage sector. Weeks earlier. By the end of the day on Friday, February 17, the tape showed a gain of $9.37 or 10.7%.

In what is being widely reported as a $143 billion offer for KHC to merge with Unilever but in reality may be a much richer offer due to the cash-and-stock nature of what is likely going to be a very complex deal, Kraft Heinz Unilever would instantly become the largest multinational corporation financially engineered by the folks at 3G Capital. And with their folksy financier Mr. Warren Buffet having recently been killing it in the post-election rally and the master Brazilian operator/dealmakers having just raised a massive new round of funding from the likes of Gisele Bundchen and Roger Federer, analysts should have most definitely been aware of the main driver of KHC stock. Yet they published their downgrade anyway. Slathered with a liberal dose of obscure acronyms just to make it sound like they knew what they were talking about.

Egg. Meet face.

This is what happens when analysts get spreadsheet blindness. They start tossing around acronyms and predictions about “trade spending efficiencies” and “synergy realization momentum” to make them sound smarter. But they’re lost in the woods and can’t see the narrative that is really driving the stock. They are being straitjacketed by the scaffolding minutiae they have built into their model. A slight decline in sales due to 3G refocusing on higher-margin brands, a 53rd week of shipments in 2015 that made comparisons tough in 2016, and… Poof!… Their spreadsheet spits out a $1.5 billion decline in earnings before interest, taxes, depreciation, and amortization (EBITDA) projections for 2018.

It’s not the most egregious error that spreadsheet risk has foisted upon the new world economic order. That honor will probably forever belong to Carmen Reinhart and Kenneth Rogoff and their paper that damned Europe to austerity and all its consequences. But jeez, you hope for better analysis to come out of these high-priced New York shops.

Whatever some spreadsheet model is telling you about KHC is simply not the reason to invest in Kraft Heinz. It never has been. Maybe they should have read this article I published on Seeking Alpha way back in October 2015. My thesis for making a long-term investment in KHC back then had everything to do with the blossoming partnership between Berkshire Hathaway and 3G Capital. As I wrote in a speculative post a couple years ago linking them with Coca-Cola (KO), the pair are out to catch some big acquisitions. Their recent investment bounty and successful round of funding only amplifies that sentiment.

Unilever is a big fish. Also, with nearly 60% of its sales coming from emerging markets, it is nearly a perfect fit for Kraft Heinz, which currently only nets 10% of its sales overseas. If it’s not going to be Unilever, as Business Insider has reported, it will be some other food-oriented multinational consumer staples company which, after it gets the “3G treatment” will almost certainly be accretive to earnings. Mondelez. Campbell Soup. Kellogg. General Mills. There are so many fish in the sea.

I like the opportunity so much that KHC is now the fourth-largest position in my retirement portfolio. Warren Buffett is the world’s greatest capital allocator. Jorge Lemann and his cohort have proven themselves to be the world’s greatest operators. The combination should continue to prove immensely beneficial for investors whatever their next target is going to be.

Since the offer came to light early on Friday, Unilever has vehemently and very publicly rejected it. But so did Anheuser-Busch when 3G first floated the idea of acquiring it. Despite a “fierce defense,” a $46.3 billion all-cash offer eventually became a $52 billion offer with a few concessions to the Busch family. These entrenched companies have legions of proud middle managers that refuse to believe that someone could run their business better than them. But 3G definitely can. And will. Combined with their lack of nostalgia over past traditions and good ‘ol boy hires, their love of zero-based budgeting and flat organizational structure offers nearly endless capex reductions. Each bloated bolt-on acquisition offers a new opportunity to wring out the excess.

And realize profits galore.

3G’s dance with SAB Miller was even more drawn out. After nearly a year of haggling, 3G via its suds acquisition vehicle AB-InBev (BUD) downed SAB Miller for $107 billion.

When 3G wants something, it usually gets it.

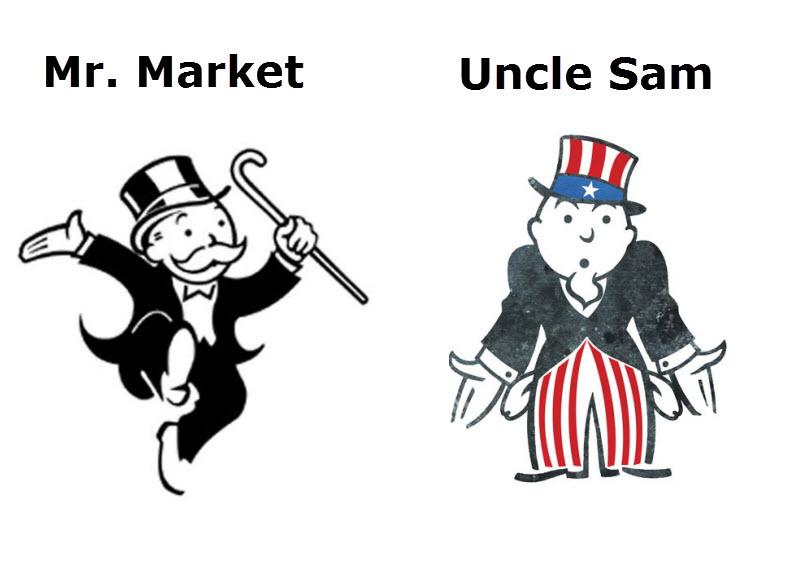

Prof. Graham asked his class to imagine a “remarkably accommodating” schizophrenic man, Mr. Market. For some reason, you find yourself a business partner of this madman. The guy is just nuts. He paces the halls throughout the day. For no reason at all and at seemingly random times, he just interjects the current prices of a wide range of securities. He doesn’t even take an hour-and-a-half break in the middle of the day like his cousin, Market Xiansheng, does in China. It’s like he’s drunk or something, kicking around the office all day yelling out numbers and pleading with just about anybody in his vicinity to buy or sell those securities he’s screaming about.

Prof. Graham asked his class to imagine a “remarkably accommodating” schizophrenic man, Mr. Market. For some reason, you find yourself a business partner of this madman. The guy is just nuts. He paces the halls throughout the day. For no reason at all and at seemingly random times, he just interjects the current prices of a wide range of securities. He doesn’t even take an hour-and-a-half break in the middle of the day like his cousin, Market Xiansheng, does in China. It’s like he’s drunk or something, kicking around the office all day yelling out numbers and pleading with just about anybody in his vicinity to buy or sell those securities he’s screaming about.